California Assembly Bill 5 Means Changes for Workers’ Compensation Insurance

California Assembly Bill 5 (also known as CA AB 5) was signed into law in September 2019, implementing a new test all employers must use to determine if a worker is an employee or an independent contractor under the California Labor Code. The law may impact who you cover under your workers’ compensation insurance policy.

While the bill is effective January 1, 2020, the part that affects workers’ compensation insurance coverage goes into effect July 1, 2020.

Know The Facts

- The new legislation is not based on policy effective date. As of July 1, 2020, as an employer, you’ll be subject to the new test. This means that a worker could be classified as an independent contractor before July 1, 2020 and as an employee after July 1, 2020.

- If you’ve employed an independent contractor that can supply you with a certificate of workers’ compensation insurance that is effective during your policy period, he/she would not be considered part of your employee roster. You would not report payroll for him/her.

- In order to avoid an unexpected change in exposures at time of audit, you must include payroll for all employees defined by the statute as of July 1, 2020.

- The statute applies to businesses headquartered in California AND businesses headquartered elsewhere with employees working in California.

Got questions? Contact me. I’m here to help you with this law change in any way possible.

-JK

Workers Compensation Insurance For Doctors

For all outpatient physician practices and clinics including physical therapists, acupuncturists, chiropractors, dialysis, x-ray laboratory services; and blood, body fluid, and tissue collection and testing.

We have a quality Workers Compensation insurance carrier applying major credits off the 8834 physicians class code. I haven’t found another carrier who can compete with them in this market.

I found this to be true for two of my clients in the past month as we marketed their workers’ compensation insurance policy renewals.

If you know of a doctor who is interested in us exploring this option on their behalf, please share this message. Now is a good time to start looking ahead at 2019 as you’re reviewing operational expenses and budgets.

-JK

The Perils of Using Unlicensed Subcontractors

All employers in the state of California that use employee labor must purchase and maintain Workers’ Compensation insurance. This requirement extends to contracting with and hiring subcontractors.

Here are some steps you can take to better manage your insurance and safety program when it comes to working with subcontractors:

Selecting A Subcontractor

Before a subcontractor begins work, confirm they are licensed and insured. You should only contract with licensed and insured subcontractors. Not having valid Workers Compensation insurance coverage renders a subcontractors license VOID. (Business and Profession Code 7152.2)

- Verify the subcontractors license: Contact the Contractors State License Board (CSLB). Visit http://www.cslb.ca.gov or call (800) 321-CSLB (2752).

- Verify the subcontractor is insured: Request a copy of their Certificate of Insurance that demonstrates Workers’ Compensation (WC) and General Liability (GL) insurance us current and active.

- Read the Certificate of Insurance and confirm the following:

- Named Insured: Verify the certificate shows the subcontractors company as the named insured.

- Types of Insurance Coverage: At a minimum they should have WC and GL coverage with limits of liability that adhere to the state minimum.

- Dates of Coverage: Make sure the policy is active, that the policy has not lapsed, and the dates extend through the end of the project or contract

- Confirm Coverage: Call the subcontractor’s agent or the insurance company to confirm information

- Request Updated Certificates of Insurance: If you work with the same subcontractors from year to year, mark your calendar to request updated certificates annually

- What if a subcontractor is unlicensed and not insured?

- “I’m a sole owner and exempt from insurance.” If this owner is working for you, most of the time they become a statutory employee and they would be covered under your Workers’ Compensation insurance policy

- Also, CA Labor Code 2750.5 presumes that an unlicensed person who performs work requiring a license is an employee and not an independent contractor. Verify licensing and insurance coverage!

What an Uninsured Subcontractor Can Cost You

- Legal Costs: The CSLB may initiate disciplinary action which may require you to hire legal counsel

- Increase in Insurance Premiums: As the uninsured subcontractor may be considered an employee, payments made to the uninsured subcontractor will be identified when your WC policy is audited resulting in additional premium.

- Claims Experience and Increased Costs: Your WC Insurance will be responsible for any injury to the subcontractor and their employees. Any claims paid under your policy will negatively affect your claims experience and all claims paid will apply to your experience modification factor three years, which can increase your insurance costs.

- Increase in Employment Taxes: You may be liable to the Employment Development Department for any unpaid contributions and tax withholding’s for the uninsured subcontractors employees

- Loss of Coverage: Under the California Insurance Code Sections 311 and 359, when an insured has misrepresented or concealed facts that are material to the application for insurance, the underwriter may rescind coverage or cancel the policy. Review your WC policy application, did you say yes or no to the use of subcontractors or sublet of work without certificates of insurance?

If you need loss control information to improve your loss prevention efforts, contact me anytime to discuss.

-JK

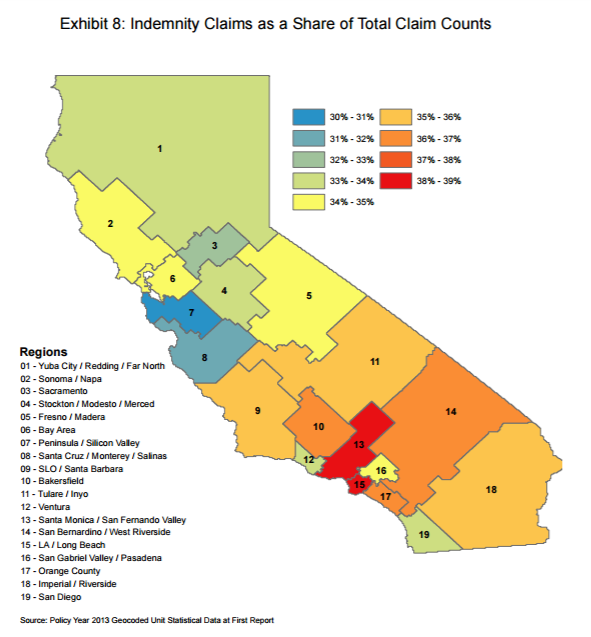

Los Angeles Has Highest Workers’ Comp Claim Costs in California

File this under the No Surprise folder but a new study by the Workers’ Compensation Insurance Rating Bureau show that Los Angeles has the highest workers’ comp claim costs in California.

Among other key findings, “The Los Angeles/Long Beach Area is the most litigious region in California. Medical legal costs are over 2.8 percent of total incurred costs on indemnity claims in the Los Angeles/Long Beach area compared with 2.0 percent statewide.”

“Indemnity claim frequencies in the Los Angeles/Long Beach area were 24.0 percent higher” than the rest of the state of California.

Read more here from the Insurance Journal:

As frustrating as this is, none of it surprises me. Not a week goes by where I don’t see a workers’ comp claim come across my desk for “cumulative trauma” or “repetitive motion” from an attorney after termination of an employee. And as I always say, nobody hurts more from this than the honest business owner trying to get by everyday running an honest business. They’re the ones paying the costs of these claims.

Here’s a map showing the regional differences of indemnity claims as a share of the total claims counts in California:

-JK

California Insurance Commissioner Awards $34.9M to Fight Workers’ Comp Fraud

Working in the Property & Casualty Insurance industry, I am happy to see the fight against Workers’ Comp Fraud. There are way too many people taking advantage of the Workers Compensation Insurance system in California, particularly Southern California. Honest business owners are stuck paying the high costs which is very much driven by those taking advantage of the system. I see it weekly with the claims coming across my desk. From the individual “claimants” to the attorneys and physicians, I hope you get caught.

-JK

Can I Be Fined for not Carrying Workers Compensation Insurance?

Answer: Yes, you can be fined for not carrying workers’ compensation insurance and more. If the Division of Labor Standards Enforcement (state labor commissioner) determines an employer is operating without workers’ compensation coverage, a stop order will be issued. This order prohibits the use of employee labor until coverage is obtained, and failure to observe it is a misdemeanor punishable by imprisonment in the county jail for up to 60 days, or by a fine of up to $10,000, or both. The Division of Labor Standards Enforcement will also assess a penalty the greater of (1) twice the amount the employer would have paid in workers’ compensation premiums during the period the employer was uninsured, determined according to subdivision (c), or (2) the sum of one thousand five hundred dollars ($1,500) per employee employed during the period the employer was uninsured. [Labor Code section 3722(b)].

Additionally, if an injured worker files a workers’ compensation claim that goes before the Workers’ Compensation Appeals Board and a judge finds the employer had not secured insurance as required by law, when the dispute is resolved the uninsured employer may be assessed a penalty of $10,000 per employee on the payroll at the time of injury if the worker’s case was found to be compensable, or $2,000 per employee on the payroll at the time of injury if the worker’s case was non-compensable, up to a maximum of $100,000. [Labor Code Section 3722(d) and (f).]

Finally, as noted in answer to a previous question, failure to secure workers’ compensation insurance is a misdemeanor punishable by imprisonment in the county jail for up to one year, or by a fine of up to ten thousand dollars ($10,000) or by both that imprisonment and fine. (Labor Code Section 3700.5)

If you need help with quotes for workers’ compensation insurance for your business, contact me today. We can market this with numerous carriers to find the best coverage and price.

-JK

Insurance For Medical Office Towers In Torrance

Just wrapped up the insurance renewals for these two medical office towers in Torrance. 140,000 Square feet

- Property Insurance

- General Liability Insurance

- Umbrella / Excess Liability Insurance

- Earthquake Insurance

- Workers’ Compensation Insurance

-JK

Top 5 Workers’ Compensation Injury Types

Data recently collected from the Bureau of Labor Statistics and the National Academy of Social Insurance shows that 65% of workers’ compensation costs can be traced to five common workplace injury types. By knowing the top five Workers’ Compensation injury types, employers can target those injuries and take action to prevent them.

Data recently collected from the Bureau of Labor Statistics and the National Academy of Social Insurance shows that 65% of workers’ compensation costs can be traced to five common workplace injury types. By knowing the top five Workers’ Compensation injury types, employers can target those injuries and take action to prevent them.

According to the data, the following are the top five injury types:

- Overexertion injuries which are caused by pushing, pulling, carrying, holding or throwing.

- Falls on the same level that may happen for a variety of reasons, such as a wet floor or a tripping hazard.

- Being struck by equipment or an object, or even a vehicle. These injuries are common in the construction industry.

- Falls to a lower level, which can be prevented by using proper fall protection, ladder safety or scaffolding.

- Other exertions or bodily reactions, which can cause strains and sprains.

A safe workplace and injury prevention are vital to keeping your workers’ compensation costs down. If your company has an increased number of claims compared to previous years, this can directly affect your experience modification factor (also known as your mod factor) and increase your workers’ compensation premium. On the other hand, decreasing your number of claims can lower your mod factor and your premium.

For more information on workplace safety, including implementing or updating a safety program in your workplace, contact me at (310) 373-6441. We have the tools to help you take control of your workers’ compensation costs.

-JK

Travelers Insurance: Insuring Technology Companies

Travelers Insurance Company has joined the ranks of other major carriers such as The Hartford in writing coverage for technology companies. Travelers Global Technology President Ronda Wescott and Chief Underwriting Officer Mike Thoma provide their perspective:

If you have a Life Science or Software and Information Technology Company and would like a review of your current insurance portfolio, feel free to contact me anytime. I can help market your coverage’s with all the major carriers specializing in this sector.

Some of the most common insurance coverage’s important to the Life Science or Software and Information Technology industry are:

- Property

- Commercial General Liability

- Professional Liability (Errors & Omissions)

- Workers’ Compensation

- Commercial Automobile

- Commercial Umbrella/ Excess Liability

- Cyber Liability & First Party Data Privacy Expense

- Directors and Officers Liability (D&O)

- Employment Practices Liability

- Fiduciary Liability

- Crime

- Kidnap and Ransom

- Group Medical Insurance

- Group Life and Disability

-JK

The Ins and Outs of Small Business Insurance

Being an entrepreneur makes you the boss, but along with getting to choose your own hours, location, and business plan, it also means that you’re responsible for a lot of other things like commercial/business insurance. There’s a lot more to business insurance than getting the lowest business insurance quotes. It means understanding your business’s unique needs and the potential hazards that can threaten its success.

This brief video from the Insurance Information Institute touches on the ins and outs of small business insurance, including coverage for:

- Property loss

- Business disruption

- Theft

- General liability (including product liability)

- Professional liability (also known as “Errors & omissions,” or “E&O”)

- Employment Practices Liability

- Workers’ Compensation

Credit: Insurance Information Institute

-JK

About Me

I’m Jimmy Kinmartin, a California licensed Property & Casualty AND Accident & Health insurance agent/broker.

I grew up in Fullerton, CA and graduated from Servite High School in Anaheim. I have my Bachelors degree from Loyola Marymount University in Los Angeles. I currently live in Tustin, CA.

Please contact me if you need help with any of the following lines of insurance for your business:

-Cyber / Data Breach

-Commercial Property

-Commercial General Liability

-Products Liability

-Workers Compensation

-Commercial Auto

-Umbrella/Excess Liability

-Errors & Omissions/ Professional Liability

-Employment Practices Liability

-Directors & Officers

-Life & Disability Insurance