Why Are My Insurance Rates Going Up??

As we’re halfway through 2013, many businesses are finding their insurance premiums increasing at renewal. This is mostly the case for workers compensation insurance here in California. We’re certainly seeing this for a majority of our clientele regardless of their industry or loss history. Calls come in asking, “why the hell is my premium going up?? I don’t have any losses and I’ve been a loyal customer paying my premiums on time for years and years.”

The property & casualty (P&C) insurance market cycle is cyclical to some extent like the real estate market. It’s characterized by periods of soft market conditions, in which premium rates are stable or falling and insurance is readily available, and by periods of hard market conditions, where rates rise, coverage may be more difficult to find and insurers’ profits increase.

The P&C insurance market has been soft over the past 6-7 years, but beware, that’s starting to change.

A driving factor in the P&C insurance market cycle is intense competition within the industry. Premium rates drop as insurance carriers compete vigorously to increase market share. As the market softens to the point that profits diminish or vanish completely, the capital needed to underwrite new business is depleted. In the up phase of the cycle, competition is less intense, underwriting standards become more stringent, the supply of insurance is limited due to the depletion of capital and, as a result, premiums rise. The prospect of higher profits draws more capital into the marketplace leading to more competition and the eventual down phase of the cycle.

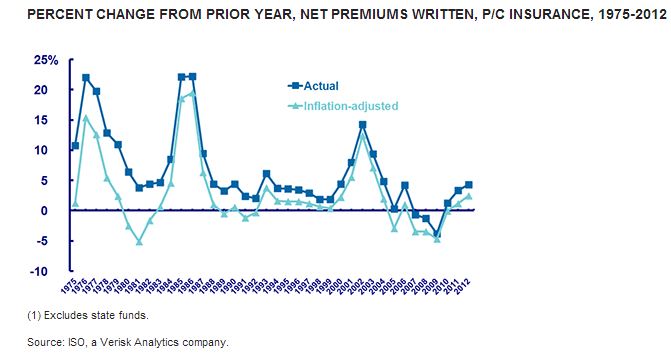

The chart below shows the real, or inflation-adjusted, growth of P&C net written premiums over more than three decades and three hard markets. This chart uses net written premiums, which reflect premium amounts after deductions for reinsurance transactions.

During the last three hard markets, inflation-adjusted net premiums written grew 7.7 percent (1975 to 1978), 10.0 percent (1984 to 1987) and 6.3 percent (2001 to 2004).

If you’re renewal premium is going up, contact your independent insurance broker to discuss ways to help curb the costs. If you’re not getting the service you expect from your broker, contact me and we can discuss your situation and review ways to find a resolution.

-JK

Credit: Insurance Information Institute

About Me

I’m Jimmy Kinmartin, a California licensed Property & Casualty AND Accident & Health insurance agent/broker.

I grew up in Fullerton, CA and graduated from Servite High School in Anaheim. I have my Bachelors degree from Loyola Marymount University in Los Angeles. I currently live in Tustin, CA.

Please contact me if you need help with any of the following lines of insurance for your business:

-Cyber / Data Breach

-Commercial Property

-Commercial General Liability

-Products Liability

-Workers Compensation

-Commercial Auto

-Umbrella/Excess Liability

-Errors & Omissions/ Professional Liability

-Employment Practices Liability

-Directors & Officers

-Life & Disability Insurance