New Smartphone App Addresses Extension Ladder Safety

Is your extension ladder positioned at an optimal and safe angle? Now it’s easier for you to figure this out with a new smartphone application the National Institute for Occupational Safety and Health (NIOSH) introduced in June.

Is your extension ladder positioned at an optimal and safe angle? Now it’s easier for you to figure this out with a new smartphone application the National Institute for Occupational Safety and Health (NIOSH) introduced in June.

Positioning extension ladders at the proper angle is critical for preventing accidents—if the ladder is set too steeply or too shallowly, it could fall. Using audio and visual signals, the Ladder Safety app provides feedback to help the user set the ladder at the best angle.

Additionally, the app provides a safety guide for extension ladder selection, inspection, accessorizing and use. Misjudging the angle at which a ladder is set is a big risk factor for falls, which are one of the leading causes of injuries for workers in any industry, especially construction.

The Ladder Safety app is free to download on both iPhone and Android devices. For more information, visit www.cdc.gov/niosh/topics/falls/.

Credit: Zywave

Why Are My Insurance Rates Going Up??

As we’re halfway through 2013, many businesses are finding their insurance premiums increasing at renewal. This is mostly the case for workers compensation insurance here in California. We’re certainly seeing this for a majority of our clientele regardless of their industry or loss history. Calls come in asking, “why the hell is my premium going up?? I don’t have any losses and I’ve been a loyal customer paying my premiums on time for years and years.”

The property & casualty (P&C) insurance market cycle is cyclical to some extent like the real estate market. It’s characterized by periods of soft market conditions, in which premium rates are stable or falling and insurance is readily available, and by periods of hard market conditions, where rates rise, coverage may be more difficult to find and insurers’ profits increase.

The P&C insurance market has been soft over the past 6-7 years, but beware, that’s starting to change.

A driving factor in the P&C insurance market cycle is intense competition within the industry. Premium rates drop as insurance carriers compete vigorously to increase market share. As the market softens to the point that profits diminish or vanish completely, the capital needed to underwrite new business is depleted. In the up phase of the cycle, competition is less intense, underwriting standards become more stringent, the supply of insurance is limited due to the depletion of capital and, as a result, premiums rise. The prospect of higher profits draws more capital into the marketplace leading to more competition and the eventual down phase of the cycle.

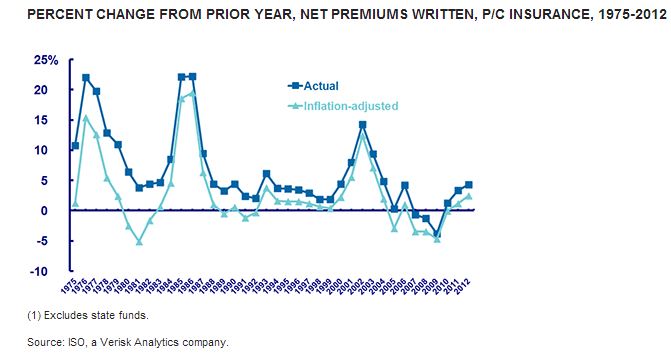

The chart below shows the real, or inflation-adjusted, growth of P&C net written premiums over more than three decades and three hard markets. This chart uses net written premiums, which reflect premium amounts after deductions for reinsurance transactions.

During the last three hard markets, inflation-adjusted net premiums written grew 7.7 percent (1975 to 1978), 10.0 percent (1984 to 1987) and 6.3 percent (2001 to 2004).

If you’re renewal premium is going up, contact your independent insurance broker to discuss ways to help curb the costs. If you’re not getting the service you expect from your broker, contact me and we can discuss your situation and review ways to find a resolution.

-JK

Credit: Insurance Information Institute

How Are Commercial Insurance Premiums Determined?

The way an insurance policy is rated determines how the policy premium is developed. Rating factors vary based on the line of insurance you are purchasing.

If you are purchasing commercial property insurance, the building rating formula is based on factors including square footage, type of construction, sprinklered or non-sprinklered, the fire protection classification, etc.

If you are purchasing commercial property insurance, the building rating formula is based on factors including square footage, type of construction, sprinklered or non-sprinklered, the fire protection classification, etc.

If you are purchasing general liability insurance, the rating formula can be based on square footage, payroll, or gross sales depending on the general liability classification codes used. These are known as rating exposures.

Once the rating exposures are identified and the deductibles selected (usually from information you have provided on the application), the premium is calculated by a simple formula: rate x exposure = premium. The deductible amount you choose will be calculated in the rate. The higher the deductible (the amount you choose to self-insure) the lower the rate. By utilizing higher deductibles, you can bring your premium cost down; however, you do not want to jeopardize your company’s financial future by choosing overly large deductibles.

Speak with your broker-agent for the deductible options available to you when purchasing commercial insurance.

The basic rating equation most often utilizes other modification factors, which can include experience modifications, schedule rating, or judgment rating. Because rating formulas can range from simple to complex, depending on the line of insurance, it is important to discuss how your policy is rated and how the policy premium is calculated with your broker-agent.

Source: California Department of Insurance

-JK

6 Reasons Why Businesses Should Use One Broker For ALL Insurance Needs

- It’s more CONVENIENT to call one office…..don’t waste your time calling several brokers to see who handles a service or claims issue.

- It’s LESS EXPENSIVE: think about multi-policy discounts and avoid buying the same coverage twice from separate brokers.

- It’s SIMPLER with combined billing statements

- It provides SECURITY to know your Account Manager has reviewed and coordinated all your policies to avoid “gaps” in your insurance protection.

- Feel COMFORTABLE knowing your insurance agent knows you personally

- It enhances CLAIMS VALUE by charging one deductible or consolidating claims with one adjuster if multiple policies are involved.

–JK

Professional Liability Insurance Coverage For Technology Businesses

Every business has unique risks that can seriously harm an organization’s operations if not properly protected against. As a business utilizing technology to produce and deliver products and/or services, it’s important to recognize and take precautions against risks that your Commercial General Liability insurance coverage does not include.

Technology Professional Liability insurance coverage, also referred to as Tech Errors and Omissions (E&O) insurance, is essential for companies using technology because it addresses a lack of protection in Commercial General Liability policies, which typically do not cover claims of third-party financial harm.

Who needs Tech E&O Coverage?

Not only technology industry businesses have technology-related risks. Most companies today utilize technology in some part of providing a service or product and need to take the necessary precautions. To ensure your company is covering all bases, a full risk management assessment is needed.

What does Tech E&O cover?

Tech E&O insurance manages risks, resulting from providing a product or service to a third party, that are not covered by a Commercial General Liability insurance policy. Specifically, Tech E&O insurance protects your business in the event that a third party suffers a financial loss due to your product or service not performing as it was intended or expected, including the event of an error or omission committed by your company. These insurance policies also cover defense costs in the event of litigation.

Tech E&O coverage would apply in the following situations:

- A mistake was made and an error in the code of a website or program your company produced isn’t found before it is implemented. A third party depends on this product or service to operate its business and its operations are stalled due to the error, causing them a financial loss.

- A part your company produces is installed in a piece of equipment. After a short amount of time, the component simply stops working, causing the equipment to fail to work, but otherwise not damaging anything or hurting anyone. The third party that relies on this equipment for its business has to stop operations and suffers a financial loss.

- An employee of your company recommends that a client make an adjustment to its network. The client follows the advice and its network crashes as a result, causing a time and financial loss for its operations.

In all of these cases, Commercial General Liability insurance coverage would not cover a claim or any costs of litigation because of the presence of an error and the lack of resulting physical damage to the third party’s property.

Contact me anytime to learn more about protecting yourself with a comprehensive professional liability insurance policy.

Credit: Zywave

Avoid the Jolt from a Lightning Bolt!

I came across this fierce 30 second video on Youtube today of a lightning bolt striking the shore of a beach about a hundred or so yards from a hotel balcony where some guy was filming. Check it out (some cursing included so beware)

The force and power are so crazy it knocked the guy back a little bit!

Living in Southern California, we don’t see a lot of intense thunder and lightning, but you should learn to identify the early signs of an oncoming thunder and lightning storm.

Typically you’ll see towering clouds in the shape of a cauliflower, dark sky, distant rumbles of thunder and flashes of lightning. When a storm is on the verge of striking your area, you need to take cover to get out of harm’s way.

Here’s how:

- Seek shelter in an enclosed building, if possible.

- If you are in a car, stay inside and keep the windows securely rolled up.

- Do not use a small shed, pavilion or lean-to as shelter; they do not provide enough protection.

- Stay several feet away from open windows, sinks, toilets, tubs, showers, electric boxes, outlets and appliances during a lightning storm. Lightning bolts can flow through these items, “jump” to you and give you a jolt.

- Do not use a landline telephone during a storm. Opt for a cellular or cordless phone, which is not connected to the building’s wiring.

If you are caught outside in a lightning storm:

- If your skin starts to tingle or your hair stands up, lightning may be about to strike. Crouch to the ground on the balls of your feet and place your feet close together. Then, place your hands on your knees and lower your head. Try to get as close to the ground as possible without placing your hands or knees on the ground.

- Avoid seeking shelter under trees, near metal fences, pipes or tall and long objects.

- If you are swimming, boating or fishing, seek shelter on land immediately.

- If you are boating and cannot get to shore before the storm hits, crouch your body down in the middle of the boat, as low as you can get.

Next time you’re in the path of a thunderstorm, you can stay cool knowing Jim Kinmartin taught you everything you need to know about dealing with it ;).

Planning is important when it comes to preparing for storms, and that includes having the proper home or business insurance. Contact your broker or me to learn more about insurance solutions for your home, business and life.

–JK

As Summer Heats Up, Put your Cellphone on “ICE”

70% of 9-1-1 calls are placed from cell phones

Today you can use your cellphone to email, take pictures, manage your calendar and even record video. However, they are still most valuable in calling for help when emergency strikes.

What can you do to prepare in case something happens to you and you can’t call for help? Entering an emergency contact in your cellphone contact list under “ICE,” which stands for In Case of Emergency, is a commonplace practice that’s helpful in the following ways:

- Most emergency responders check cellphones for an ICE entry, which enables them to quickly contact your loved ones in an emergency.

- Provides peace of mind for parents with children, knowing you’ll be contacted first in an emergency situation.

Don’t delay: Add “ICE” to you cellphone contact list today!

Credit: Zywave, Inc.

–JK

How far has car safety come in 50 years? Take a look

1959 Chevrolet Bel Air vs. 2009 Chevrolet Malibu car safety crash test.

In the 50 years since US insurers organized the Insurance Institute for Highway Safety, car crashworthiness has improved. Demonstrating this was a crash test conducted between a 1959 Chevrolet Bel Air and a 2009 Chevrolet Malibu. In a real-world collision similar to this test, occupants of the new model would fare much better than in the vintage Chevy.

“It was night and day, the difference in occupant protection,” says Institute president Adrian Lund. “What this test shows is that automakers don’t build cars like they used to. They build them better.”

The crash test was conducted at an event to celebrate the contributions of auto insurers to highway car safety progress over 50 years. Beginning with the Institute’s 1959 founding, insurers have maintained the resolve, articulated in the 1950s, to “conduct, sponsor, and encourage programs designed to aid in the conservation and preservation of life and property from the hazards of highway accidents.”

More information at http://www.iihs.org/50th/default.html

–JK

Happy Small Business Week 2013

This year marks the 50th anniversary of National Small Business Week. Every year since 1963, the President of the United States has issued a proclamation announcing National Small Business Week, which recognizes the critical contributions of America’s entrepreneurs and small business owners.

More than half of Americans either own or work for a small business, and they create about two out of every three new jobs in the U.S. each year. Small businesses have always been the backbone of our economy, and we know that the success of America’s small businesses is critical to growing our economy and increasing our nation’s global competitiveness.

Small businesses create two out of three net new private sector jobs in our economy. And today, half of all working Americans either own or work for a small business.

To all of the small businesses out there, this week is about you. Happy Small Business Week!

–JK

About Me

I’m Jimmy Kinmartin, a California licensed Property & Casualty AND Accident & Health insurance agent/broker.

I grew up in Fullerton, CA and graduated from Servite High School in Anaheim. I have my Bachelors degree from Loyola Marymount University in Los Angeles. I currently live in Tustin, CA.

Please contact me if you need help with any of the following lines of insurance for your business:

-Cyber / Data Breach

-Commercial Property

-Commercial General Liability

-Products Liability

-Workers Compensation

-Commercial Auto

-Umbrella/Excess Liability

-Errors & Omissions/ Professional Liability

-Employment Practices Liability

-Directors & Officers

-Life & Disability Insurance