The Ins and Outs of Small Business Insurance

Being an entrepreneur makes you the boss, but along with getting to choose your own hours, location, and business plan, it also means that you’re responsible for a lot of other things like commercial/business insurance. There’s a lot more to business insurance than getting the lowest business insurance quotes. It means understanding your business’s unique needs and the potential hazards that can threaten its success.

This brief video from the Insurance Information Institute touches on the ins and outs of small business insurance, including coverage for:

- Property loss

- Business disruption

- Theft

- General liability (including product liability)

- Professional liability (also known as “Errors & omissions,” or “E&O”)

- Employment Practices Liability

- Workers’ Compensation

Credit: Insurance Information Institute

-JK

Smart Phone Captures the Poinsettia Fire Burning in Carlsbad

WARNING: GRAPHIC LANGUAGE

In Carlsbad, officials said at a news briefing that 22 housing structures were destroyed: four single-family homes and an 18-unit apartment building, along with two commercial buildings. The loss was estimated at $22.5 million according to the L.A. Times.

-JK

California Is Riskiest State for Employee Lawsuits

A new study by Hiscox revealed that, on average, a United States-based business with at least 10 employees has a 12.5% chance of having an employment liability charge filed against them. However, California has the most frequent incidences of Employment Practices Liability charges in the country and businesses in the state have a 42% higher chance of being sued by an employee than the national average! Not surprising!

Behind California, #2 is Illinois, #3 – Alabama, #4 – Arizona & Mississippi. and #5 is Georgia.

The Hiscox survey reveals that lower-risk states for Employment Practices Liability charges include Massachusetts, Michigan, Kentucky, Washington and West Virginia.

One way to help mitigate loss from an employee, potential employee, or former employee suing your business for an employment related claim is to purchase an Employment Practices Liability Insurance policy. Workers Compensation Insurance does NOT cover Employment Practices Liability related claims!

-JK

Source – PropertyCasualty360

Dramatic Rescue of Construction Worker From Blaze

A construction worker is rescued from a giant fire at AIG campus in Houston, Texas, on Tuesday. The amateur footage, filmed by onlooker Karen Jones, shows a man trapped on a top-floor balcony of an apartment complex that had been under construction. He manages to escape as fire destroys the building. No injuries were reported as a result of the blaze. It is still unclear what caused the fire. You’ll get some sweaty palms watching this one! Especially when the construction worker swings down to the lower level balcony!

-JK

Forklift Operator Knocks Over $100,000 Worth of Liquor

As seen in this Youtube video, “in a Russian liquor warehouse, a forklift driver hits the gas in reverse and plows into a warehouse rack filled with liquor, causing a domino effect that brings down half the warehouse. There was over a hundred thousand dollars in damage. The driver survived. No report if he is still employed.”

All joking aside, an accident like this can have a vast impact on your business operations such as Property Damage with the destroyed product. Think about the extensive clean up and reorganization; the suspense of business operations/ business income/interruption exposure. Also, from a Workers Compensation and Employee Disability standpoint, there are injured employees which means lost time, recovery, employee shortage, and training costs for other employees to fill the void. This can have a devastating impact on your bottom line.

Here are some Safety Tips For Forklift Drivers:

Maintenance

- Each day, check that the forklift is ready for the day’s work and perform any necessary maintenance before operating.

- Report any malfunction or poor performance to your supervisor immediately.

Loading

- Use reverse when going down inclines and go forward up inclines.

- Do not travel with the load elevated, and keep the load stable and as close to the floor as possible.

- Avoid raising or lowering a load while the forklift is moving.

- Always keep the load tilted back towards the carriage while raising and lowering.

- Make sure the load is balanced and is within the capacity of the truck.

- Never use the forks as a personnel elevator unless properly equipped.

Driving

- Always make sure your driving path is clear.

- Slow down for corners, blind spots and doorways.

- Drive defensively by always being aware of your surroundings and watching for the unexpected.

- Be aware of ground conditions and always take the smoothest possible path.

- Never try to turn on an incline.

- Cross tracks diagonally and slow down for uneven surfaces.

- Keeps legs, arms, feet, hands and head inside the forklift.

- Be aware of others around the job site, in case they do not see you.

- Always give those on foot the right of way.

- Stay out from under forks and loads.

- Never show off or use the machine for anything other than your specified job tasks.

- Never give anyone a ride or allow anyone who is untrained to operate the forklift.

Finally, here’s a Sample Performance Test for Forklift Operators for reference to monitor your employee forklift drivers.

Minimize, monitor, and control the probability and/or impact of unfortunate events before they happen. That’s what Risk Management is all about.

-JK

Top 10 U.S. Business Risks for 2014

According to the “Allianz Risk Barometer,” a survey from Allianz Global Corporate & Specialty SE, the top 10 U.S. Business Risks are:

- Business interruption, supply chain (61 percent)

- Natural catastrophes (58 percent)

- Fire/explosion (24 percent)

- Loss of reputation, brand value (17 percent)

- Cyber crime, IT failure, espionage (15 percent)

- Intensified competition (12 percent)

- Quality deficiencies, serial defects (10 percent)

- Environmental changes (10 percent)

- Changes in legislation and regulation (10 percent)

- Market stagnation or decline (10 percent)

Loss of reputation or brand value joined the top 10 list, and was the fourth ranked business risk as cited by U.S. companies. Cybercrime, including IT failures and espionage, were No. 5. Those rankings were lower for non-U.S. companies, which ranked cyber at No. 8 and loss of reputation at No. 6.

Source: Insurance Networking News

-JK

Powerful Driving-Safety Ad

This powerful and simple driving safety advertisement from the New Zealand Transport Agency will really make you think about speeding and will probably give you some serious goosebumps when you watch it.

From Mashable: the public-service announcement dissects an accident by freezing the moment before impact. A man who pulled out of an intersection too fast pleads for his life and that of his son. The request falls on deaf ears, though. “I’m going too fast,” replies the driver of the oncoming car. The point: Other drivers make mistakes, too, so be careful.

Take a look for yourself:

Be careful out there and make sure you think of others first before yourself when you’re running late for that party, for work, or wherever else you’re trying get to. Give yourself plenty of time so that you’re not putting yourself in the situation where you feel the need to speed.

-JK

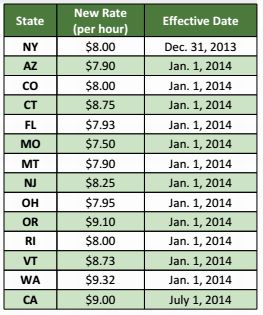

Minimum Wage Increases for 2014

As of December 1, 2013, 14 states, including California, have announced an increase in their minimum wage rate. In addition to California, these states are: New York, Arizona, Colorado, Connecticut, Florida, Missouri, Montana, New Jersey, Ohio, Oregon, Rhode Island, Vermont, and Washington.

Employers in these states should review their employees’ wage payment rates and update their minimum wage poster requirements as necessary to ensure their compliance with state regulations.

Here are the 2014 minimum wage rates for all of these states:

-JK

-JK

New High-tech Auto Theft Device Showing Up In The U.S.

From Long Beach, CA to Chicago, IL, thieves with no keys are breaking into automobiles with mysterious new high-tech hand-held box device. It appears this is the latest high-tech crime tool as cars have become “rolling computers.” Check out this news piece from CNN which was originally published on 6/21/13.

According to the California Highway Patrol, there were more than 700,000 auto thefts nationwide in 2011, with 156,796 occurring in California, the most for any state.

It’s important to know what to do if your vehicle is stolen. Here are a few suggestions:

1 – The best offense is a good defense. Consider purchasing comprehensive car insurance, which covers your vehicle if it is damaged in anything other than a collision. This includes auto theft, vandalism, floods, hailstorms and fire damage.

2 – Contact police immediately if your vehicle is stolen and file a report. The chances of recovering a stolen vehicle decreases as time passes.

3 – Be sure to have the following information when filing a claim with your insurance carrier:

- Policy number

- When and where you last saw your car (date, time and location)

- Year, make and model

- Vehicle identification number

- License plate number

- Police report number

4 – Be sure to list any additional valuables that were in your car at the time it was stolen.

5 – Offer photos of your car, if possible, to the police and your claims adjuster.

-JK

There Is Always Someone Who Will Do It Cheaper

I saw this photo and caption surfing my LinkedIn home page, so I don’t know who to give credit to on this one, but had to share. I think pretty much any human can identify with this one:

This totally reminds me of the insurance industry, especially personal auto insurance. Every commercial you see on TV is along the lines of “give us 15 minutes and we’ll save you 15% on your car insurance.” Or, “you can save hundreds on your car insurance.”

Well, maybe you can, but at what costs when you actually need the coverage? Instead of looking at the bottom line only, know what value you’re getting on what you’re buying. I don’t care if it’s the sprinkler repair guy, rain gutter installation, home remodeling, or insurance, is cheaper always better in the long run? Or, just more time, money, and headaches in the future?

Don’t believe everything you see from the surface. Have a need? Talk to a friend and see they have had a good experience with someone they can recommend. Then you can have the peace of mind knowing you’re getting the best VALUE for what you’re buying.

My go-to quote from Oscar Wilde sums it all up: “Nowadays people know the price of everything and the value of nothing”

-JK

About Me

I’m Jimmy Kinmartin, a California licensed Property & Casualty AND Accident & Health insurance agent/broker.

I grew up in Fullerton, CA and graduated from Servite High School in Anaheim. I have my Bachelors degree from Loyola Marymount University in Los Angeles. I currently live in Tustin, CA.

Please contact me if you need help with any of the following lines of insurance for your business:

-Cyber / Data Breach

-Commercial Property

-Commercial General Liability

-Products Liability

-Workers Compensation

-Commercial Auto

-Umbrella/Excess Liability

-Errors & Omissions/ Professional Liability

-Employment Practices Liability

-Directors & Officers

-Life & Disability Insurance