Video From Cockpit of A plane Fighting the Rim Fire in Yosemite

Look at this unreal footage of the Rim Fire in Yosemite, California, taken from the cockpit of an Air National Guard plane:

Hot and dry weather conditions are well-known risk factors for forest fires. A majority of the forest fires are caused by a combination of these conditions and careless human activity.

Officials expect some regions of the country like California to be at a higher risk for forest fires than usual due to low moisture and rising temperatures.

Here are some tips to keep top of mind when choosing a site to start a fire:

- Check to see if open fires are allowed in your area.

- Choose an area with an abundance of rocks and sand and little vegetation.

- Do not start a fire underneath low hanging branches or nearby bushes.

- Have plenty of water nearby in case the fire gets out of hand.

- Keep the fire small.

- Never wander away from a fire; it should be watched and kept under control at all times.

-JK

Aerial Firefighting

This is a pretty cool video of a helicopter maneuvering in someone’s backyard to scoop up water from a pool to help fight a wildfire.

Planes and helicopters are critical tools in managing wildfires, particularly in California where we face wildfires annually. Although aircraft are often used to fight wildfires, aircraft alone cannot put them out. Firefighters rely on planes and helicopters to:

- Deliver equipment and supplies.

- Deploy smokejumpers and rappellers to a fire.

- Transport firefighters.

- Provide reconnaissance of new fires, fire locations, and fire behavior.

- Drop fire-retardant or water to slow down a fire so firefighters can contain it.

- Ignite prescribed fires

Thanks to all our fire service personnel who help protect us when we need it. We are grateful to have them.

Source: US Fire Service

Scary Tornado Sirens in Chicago

Listen to these Tornado Sirens in downtown Chicago from 2008 apparently

What do you during a tornado? Well…Getting off a tall building would be job one.

Here’s an instructional guide to learn what to do before, during and after a tornado: (Tornadoes). <— Click here and feel free to share with others.

Luckily, tornadoes aren’t something we have to worry about much here in California. Unfortunately, earthquakes are.

-JK

New Smartphone App Addresses Extension Ladder Safety

Is your extension ladder positioned at an optimal and safe angle? Now it’s easier for you to figure this out with a new smartphone application the National Institute for Occupational Safety and Health (NIOSH) introduced in June.

Is your extension ladder positioned at an optimal and safe angle? Now it’s easier for you to figure this out with a new smartphone application the National Institute for Occupational Safety and Health (NIOSH) introduced in June.

Positioning extension ladders at the proper angle is critical for preventing accidents—if the ladder is set too steeply or too shallowly, it could fall. Using audio and visual signals, the Ladder Safety app provides feedback to help the user set the ladder at the best angle.

Additionally, the app provides a safety guide for extension ladder selection, inspection, accessorizing and use. Misjudging the angle at which a ladder is set is a big risk factor for falls, which are one of the leading causes of injuries for workers in any industry, especially construction.

The Ladder Safety app is free to download on both iPhone and Android devices. For more information, visit www.cdc.gov/niosh/topics/falls/.

Credit: Zywave

Huge Thunder Storm In Japan; Train Takes A Direct Hit

We don’t see thunder and lightning like this in Southern California! Watch this train get struck by lightning at the 1:20 mark in the video:

When a lightning storm is on the verge of striking your area, you need to take cover to get out of harm’s way. Here are some tips from a former post on Lightning Safety Considerations

-JK

Why Are My Insurance Rates Going Up??

As we’re halfway through 2013, many businesses are finding their insurance premiums increasing at renewal. This is mostly the case for workers compensation insurance here in California. We’re certainly seeing this for a majority of our clientele regardless of their industry or loss history. Calls come in asking, “why the hell is my premium going up?? I don’t have any losses and I’ve been a loyal customer paying my premiums on time for years and years.”

The property & casualty (P&C) insurance market cycle is cyclical to some extent like the real estate market. It’s characterized by periods of soft market conditions, in which premium rates are stable or falling and insurance is readily available, and by periods of hard market conditions, where rates rise, coverage may be more difficult to find and insurers’ profits increase.

The P&C insurance market has been soft over the past 6-7 years, but beware, that’s starting to change.

A driving factor in the P&C insurance market cycle is intense competition within the industry. Premium rates drop as insurance carriers compete vigorously to increase market share. As the market softens to the point that profits diminish or vanish completely, the capital needed to underwrite new business is depleted. In the up phase of the cycle, competition is less intense, underwriting standards become more stringent, the supply of insurance is limited due to the depletion of capital and, as a result, premiums rise. The prospect of higher profits draws more capital into the marketplace leading to more competition and the eventual down phase of the cycle.

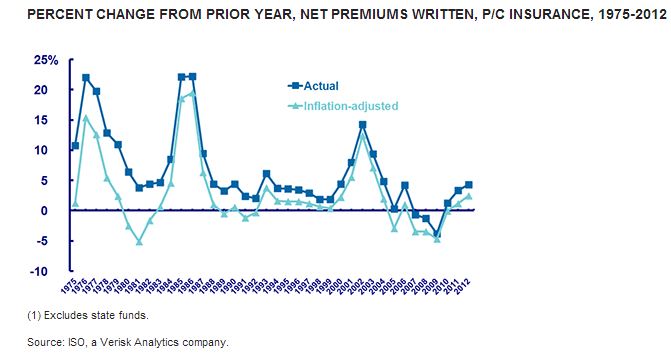

The chart below shows the real, or inflation-adjusted, growth of P&C net written premiums over more than three decades and three hard markets. This chart uses net written premiums, which reflect premium amounts after deductions for reinsurance transactions.

During the last three hard markets, inflation-adjusted net premiums written grew 7.7 percent (1975 to 1978), 10.0 percent (1984 to 1987) and 6.3 percent (2001 to 2004).

If you’re renewal premium is going up, contact your independent insurance broker to discuss ways to help curb the costs. If you’re not getting the service you expect from your broker, contact me and we can discuss your situation and review ways to find a resolution.

-JK

Credit: Insurance Information Institute

How Are Commercial Insurance Premiums Determined?

The way an insurance policy is rated determines how the policy premium is developed. Rating factors vary based on the line of insurance you are purchasing.

If you are purchasing commercial property insurance, the building rating formula is based on factors including square footage, type of construction, sprinklered or non-sprinklered, the fire protection classification, etc.

If you are purchasing commercial property insurance, the building rating formula is based on factors including square footage, type of construction, sprinklered or non-sprinklered, the fire protection classification, etc.

If you are purchasing general liability insurance, the rating formula can be based on square footage, payroll, or gross sales depending on the general liability classification codes used. These are known as rating exposures.

Once the rating exposures are identified and the deductibles selected (usually from information you have provided on the application), the premium is calculated by a simple formula: rate x exposure = premium. The deductible amount you choose will be calculated in the rate. The higher the deductible (the amount you choose to self-insure) the lower the rate. By utilizing higher deductibles, you can bring your premium cost down; however, you do not want to jeopardize your company’s financial future by choosing overly large deductibles.

Speak with your broker-agent for the deductible options available to you when purchasing commercial insurance.

The basic rating equation most often utilizes other modification factors, which can include experience modifications, schedule rating, or judgment rating. Because rating formulas can range from simple to complex, depending on the line of insurance, it is important to discuss how your policy is rated and how the policy premium is calculated with your broker-agent.

Source: California Department of Insurance

-JK

Drunk Driver Nearly Causes Multiple Accidents – Ends Up Crashing

Check out this cliff-hanger video. This drunk driver nearly causes multiple accidents but ends up crashing and putting his/her own life in jeopardy. Some tense moments on this two lane highway!

According to Mothers Against Drunk Driving (MADD), out of every three traffic deaths involve drunk driving. Every 53 minutes on average, someone is killed in a drunk driving crash (9,878 people in total in 2011). Every 90 seconds, someone is injured because of this entirely preventable crime.

About one-third of the drunk driving problem – arrests, crashes, deaths, and injuries – comes from repeat offenders. At any given point we potentially share the roads with 2 million people with three or more drunk driving offenses.

What to do when you spot an Impaired Driver

- Stay far behind the suspected drunk driver.

- Get out of the way and expect the unexpected.

- Wear your safety belt (and make sure that any children or other passengers have their safety belts fastened as well) – It is one of your best defenses against a drunk driver.

- Stop right away and look for a phone.

- Report suspected and impaired drivers to the California Highway Patrol or local police by dialing 911. Give the location, direction of travel, and description of the car and driver’s behavior.

What NOT to do when you spot an Impaired Driver

- Do not try to pass the car!

- Do not try to stop the vehicle.

- Do not follow too closely. The car may stop abruptly.

- Do not attempt to act in the capacity of the police.

- Do not try to detain or confront the driver.

- Call the local police or 911 and let them take care of it!

Most of the time, the signs of a drunk driver aren’t as obvious as the white Ranger in this video. Stay alert on the roads out there!

–JK

6 Reasons Why Businesses Should Use One Broker For ALL Insurance Needs

- It’s more CONVENIENT to call one office…..don’t waste your time calling several brokers to see who handles a service or claims issue.

- It’s LESS EXPENSIVE: think about multi-policy discounts and avoid buying the same coverage twice from separate brokers.

- It’s SIMPLER with combined billing statements

- It provides SECURITY to know your Account Manager has reviewed and coordinated all your policies to avoid “gaps” in your insurance protection.

- Feel COMFORTABLE knowing your insurance agent knows you personally

- It enhances CLAIMS VALUE by charging one deductible or consolidating claims with one adjuster if multiple policies are involved.

–JK

Professional Liability Insurance Coverage For Technology Businesses

Every business has unique risks that can seriously harm an organization’s operations if not properly protected against. As a business utilizing technology to produce and deliver products and/or services, it’s important to recognize and take precautions against risks that your Commercial General Liability insurance coverage does not include.

Technology Professional Liability insurance coverage, also referred to as Tech Errors and Omissions (E&O) insurance, is essential for companies using technology because it addresses a lack of protection in Commercial General Liability policies, which typically do not cover claims of third-party financial harm.

Who needs Tech E&O Coverage?

Not only technology industry businesses have technology-related risks. Most companies today utilize technology in some part of providing a service or product and need to take the necessary precautions. To ensure your company is covering all bases, a full risk management assessment is needed.

What does Tech E&O cover?

Tech E&O insurance manages risks, resulting from providing a product or service to a third party, that are not covered by a Commercial General Liability insurance policy. Specifically, Tech E&O insurance protects your business in the event that a third party suffers a financial loss due to your product or service not performing as it was intended or expected, including the event of an error or omission committed by your company. These insurance policies also cover defense costs in the event of litigation.

Tech E&O coverage would apply in the following situations:

- A mistake was made and an error in the code of a website or program your company produced isn’t found before it is implemented. A third party depends on this product or service to operate its business and its operations are stalled due to the error, causing them a financial loss.

- A part your company produces is installed in a piece of equipment. After a short amount of time, the component simply stops working, causing the equipment to fail to work, but otherwise not damaging anything or hurting anyone. The third party that relies on this equipment for its business has to stop operations and suffers a financial loss.

- An employee of your company recommends that a client make an adjustment to its network. The client follows the advice and its network crashes as a result, causing a time and financial loss for its operations.

In all of these cases, Commercial General Liability insurance coverage would not cover a claim or any costs of litigation because of the presence of an error and the lack of resulting physical damage to the third party’s property.

Contact me anytime to learn more about protecting yourself with a comprehensive professional liability insurance policy.

Credit: Zywave

About Me

I’m Jimmy Kinmartin, a California licensed Property & Casualty AND Accident & Health insurance agent/broker.

I grew up in Fullerton, CA and graduated from Servite High School in Anaheim. I have my Bachelors degree from Loyola Marymount University in Los Angeles. I currently live in Tustin, CA.

Please contact me if you need help with any of the following lines of insurance for your business:

-Cyber / Data Breach

-Commercial Property

-Commercial General Liability

-Products Liability

-Workers Compensation

-Commercial Auto

-Umbrella/Excess Liability

-Errors & Omissions/ Professional Liability

-Employment Practices Liability

-Directors & Officers

-Life & Disability Insurance