REMINDER: Post your OSHA Log Summary by Feb. 1

It’s that time of year again—Feb. 1 marks the deadline for you to tabulate your annual OSHA Log Summary (OSHA Form 300A) and post it in a common area wherever notices to employees are usually posted.

The summary must list the total number of job-related injuries and illnesses that occurred in calendar year 2013 and logged on the OSHA 300 Form. And don’t forget to leave the Summary posted until April 30, 2014.

If you need additional assistance, have questions about recordability, or would like to compare your loss performance trends against national benchmarking data, contact me today for more information.

-JK

Insurance For a Men’s Retail Clothing Store

I spent some time this Saturday morning working up some insurance quotes and options for a new men’s clothing retail store opening this Fall in Laguna Beach (CA). We’re looking into property, general liability, and workers’ compensation insurance coverage for the store.

Since my brain is on the subject of insurance for retail clothing stores, i wanted to share a brief risk summary that you should think about if you own a retail clothing store.

Since my brain is on the subject of insurance for retail clothing stores, i wanted to share a brief risk summary that you should think about if you own a retail clothing store.

Property exposures are limited, but if a fire should occur, the clothing provides a combustible fire load and is highly susceptible to water and smoke damage. Theft may be a concern if any of the items sold have high value. Appropriate security measures should be in place.

Crime exposures are from Employee Dishonesty and Theft of Money and Securities either from holdup or safe burglary. Employee dishonesty is controlled through inventory monitoring, control of the cash register, disciplined controls and division of duties. Theft prevention requires controls of monies kept in the cash drawers and regular bank drops.

Premises liability is always a concern in a retail exposure where the public comes to the premises. Floor covering must be in good condition with no frayed or worn spots on carpet and no cracks or holes in flooring. Sufficient exits must be provided and be well-marked, with backup systems in case of power failure. Dressing rooms must be well maintained and privacy carefully guarded. Shoplifting procedures must be fully understood and utilized by all employees.

Parking lots and sidewalks need to be in good repair with snow and ice removed, and generally level and free of exposure to slip and fall. If the business is open after dark, adequate lighting and appropriate security for the area must be present.

Products liability for this type of operation is normally low. Direct importing of clothes and tailoring can add to the exposure.

Workers compensation exposure is from lifting, which can cause back injury, hernia, sprain, and strain. What kind of training do employees receive, and what types of material lifting or conveying devices are used? If tailoring services are offered, injuries due to sewing and cutting injuries are possible.

Minimum recommended coverage:

Business Personal Property, Business Income, Employee Dishonesty, Money and Securities, Accounts Receivable, Computers, General Liability, Employee Benefits, Umbrella, Hired and Nonownership Auto, Workers Compensation. Many of these coverage’s can be included within a single Businessowners insurance policy.

Other coverages to consider:

Building, Leasehold Interest, Real Property Legal Liability, Forgery, Computer Fraud, Bailees Customers, Fine Arts, Employment Related Practices, Business Auto Liability and Physical Damage.

Have a retail clothing store and need some guidance on your insurance? You can contact me anytime to discuss. I’d be happy to help you out.

-JK

Source: Rough Notes, Inc

The Cost of NOT Buying Insurance. A True Story

Last week I got a phone call from a guy (a business owner) who sounded totally panicked. I could hear it in his voice immediately. Panicked about the need for workers’ compensation insurance. The conversation started casually,

“Um, yeah, we need a workers’ compensation insurance policy to cover our employees.”

We talk for a bit as I try to get an understanding of his current situation.

“Well it was something we kind of, um, overlooked over the past couple years.”

“Past couple years?” I ask. “So why are you suddenly looking for a policy now?”

Still no direct answer.

“Have you had any claims or losses in the past 3 years?” I ask.

I didn’t need to ask much more.

“Yes, I received notification from an attorney about a former employee of mine.”

The business, a retail bakery, received a letter from an attorney in the mail. It turns out a former employee who quit over a month ago dropped a bomb with a claim for cumulative trauma to the feet, back, neck, knees.

So here this business is at a point with a serious issue to contend with. They didn’t buy workers compensation insurance policy when they first hired employees. Their reasoning was they just didn’t want to incur the costs and figured this could never happen to them.

As an insurance resource partner, I hear this way too often from prospective clients trying to save money on insurance. Not just for workers compensation insurance either. This is for all lines of insurance like general liability, errors & omissions, property, etc.

Buying a workers compensation policy now will not do anything to help this business for a loss that has already occurred. You cannot buy a workers compensation policy with retroactive coverage. That’s like buying a health insurance policy after getting sick. This retail bread bakery is going to have deal with this claim on their own, without the support of insurance.

As if the day-to-day stress of operating a business isn’t enough, throwing this claim into the mix is sure to make things much more challenging from both a time and cost standpoint.

It doesn’t end here. In addition to handling this claim on their own, finding workers compensation insurance coverage at a reasonable cost moving forward with a standard carrier is going to be pretty much impossible. Any underwriter who sees a business with active employees and no insurance for over two years AND a claim?? No way. Costs now will be more than they would have ever paid if they secured insurance before they hired new employees.

Another potential problem this business could face is:

“It is a criminal offense for an employer to be unlawfully uninsured regardless of whether or not an employee is injured. California Labor Code Section 3700.5 specifies that it is a misdemeanor punishable by either a fine of up to $10,000 or imprisonment in the county jail for up to one year, or both. In addition, the state issues penalties of up to $100,000 against illegally uninsured employers. If an employee is injured, the employer is responsible for paying all benefits and may be subject to additional liability.”

So I ask you business owners out there, are you avoiding buying insurance because you feel it costs too much? Are you one of those who think a loss will never happen to you?

Well I recommend you think again. If this scenario isn’t enough to get you to think twice, there’s probably not a whole lot more that will. Put yourself in this business owners shoes. How much do they wish now that they were paying a workers compensation premium over the past two years for a policy to help now when they need it most?

It will be interesting to see how things pan out for this business, but one thing’s for sure, this mistake could put them out of business for good depending on the ultimate severity of the claim.

Can you afford to not carry insurance? The cost of not buying it in some form or another could be the demise of your business and livelihood depending on the severity of a loss.

-JK

Fall Protection and Safety

Five construction workers are killed from falls each week in the U.S., according to new data from the Census of Fatal Occupational Injuries (CFOI).

Watch this new video from the California State Compensation Insurance Fund with expert instructions on proper harnessing techniques to protect workers from falls and reduce risk of injuries on construction sites. Topics include: A, B, C, D of Fall Protection, inspection of Body Harness, using the correct type of connector and de-accelerating devices.:

Do you have a Fall Protection safety program established for your business? If no, you can contact me and I can help you establish one.

For a few more pointers on Fall Protection and Safety, click here: Safety Matters Fall Protection and Safety

-JK

New Smartphone App Addresses Extension Ladder Safety

Is your extension ladder positioned at an optimal and safe angle? Now it’s easier for you to figure this out with a new smartphone application the National Institute for Occupational Safety and Health (NIOSH) introduced in June.

Is your extension ladder positioned at an optimal and safe angle? Now it’s easier for you to figure this out with a new smartphone application the National Institute for Occupational Safety and Health (NIOSH) introduced in June.

Positioning extension ladders at the proper angle is critical for preventing accidents—if the ladder is set too steeply or too shallowly, it could fall. Using audio and visual signals, the Ladder Safety app provides feedback to help the user set the ladder at the best angle.

Additionally, the app provides a safety guide for extension ladder selection, inspection, accessorizing and use. Misjudging the angle at which a ladder is set is a big risk factor for falls, which are one of the leading causes of injuries for workers in any industry, especially construction.

The Ladder Safety app is free to download on both iPhone and Android devices. For more information, visit www.cdc.gov/niosh/topics/falls/.

Credit: Zywave

Why Are My Insurance Rates Going Up??

As we’re halfway through 2013, many businesses are finding their insurance premiums increasing at renewal. This is mostly the case for workers compensation insurance here in California. We’re certainly seeing this for a majority of our clientele regardless of their industry or loss history. Calls come in asking, “why the hell is my premium going up?? I don’t have any losses and I’ve been a loyal customer paying my premiums on time for years and years.”

The property & casualty (P&C) insurance market cycle is cyclical to some extent like the real estate market. It’s characterized by periods of soft market conditions, in which premium rates are stable or falling and insurance is readily available, and by periods of hard market conditions, where rates rise, coverage may be more difficult to find and insurers’ profits increase.

The P&C insurance market has been soft over the past 6-7 years, but beware, that’s starting to change.

A driving factor in the P&C insurance market cycle is intense competition within the industry. Premium rates drop as insurance carriers compete vigorously to increase market share. As the market softens to the point that profits diminish or vanish completely, the capital needed to underwrite new business is depleted. In the up phase of the cycle, competition is less intense, underwriting standards become more stringent, the supply of insurance is limited due to the depletion of capital and, as a result, premiums rise. The prospect of higher profits draws more capital into the marketplace leading to more competition and the eventual down phase of the cycle.

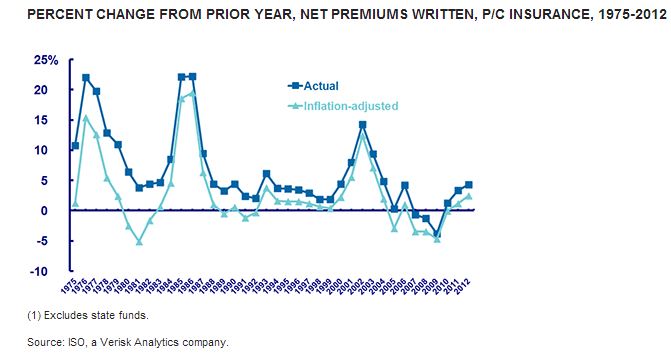

The chart below shows the real, or inflation-adjusted, growth of P&C net written premiums over more than three decades and three hard markets. This chart uses net written premiums, which reflect premium amounts after deductions for reinsurance transactions.

During the last three hard markets, inflation-adjusted net premiums written grew 7.7 percent (1975 to 1978), 10.0 percent (1984 to 1987) and 6.3 percent (2001 to 2004).

If you’re renewal premium is going up, contact your independent insurance broker to discuss ways to help curb the costs. If you’re not getting the service you expect from your broker, contact me and we can discuss your situation and review ways to find a resolution.

-JK

Credit: Insurance Information Institute

What To Do In the Event of An Insurance Claim

When you deal with an incident that gives rise to an insurance claim, it’s usually a pretty crappy situation. It can be stressful, terrifying, frightening, and alarming in many cases. First things first, try not to panic. Hopefully it’s an incident you carry insurance for to be protected.

Your insurance contract requires that you report all claims promptly. Contact your insurance carrier or broker as possible after a property, liability, worker’s comp or automobile claim. An insurance company claims adjuster will be assigned to handle your claim. You should then be able to deal directly with the adjuster to settle your claim, but your broker can be there with you to assist you along the way.

Here’s step-by-step suggestions on how you should handle property, liability, workers compensation, and auto insurance claims.

Property Claims

In the event of damage to your building or contents:

- Protect the property from further damage:

- Call the proper authorities and utilities (gas, electric, telephone).

- Take photos of the damage before having emergency repairs made, such as boarding up windows or covering holes in the roof.

- Call your insurance broker or carrier to report the loss.

- Call a contractor to estimate the building damages.

- Separate damaged contents from undamaged contents. Do not discard any items until the claims adjuster gives you the authority to do so.

- Keep records of expenses if you are forced to temporarily relocate your business.

- Do not authorize repairs until the claims adjuster has given you the authority to do so.

After the claim is reported to the insurance company, the claims adjuster will:

- Contact you by phone or mail to discuss the loss

- Arrange for an appraiser to inspect extensively damaged property

- Assist you with your choice of contractors to make the repairs

- Contact you for a settlement

Liability Claims

In the event of injuries or damage to property of others which you allegedly caused:

- Call your insurance broker or carrier to report the claim.

- Forward any correspondence, including a summons from an attorney representing the other party.

- Do not discuss the claim with the other party or their attorney. Refer them to your insurance company’s claims adjuster or to us.

After the claim is reported to the insurance company, the claims adjuster will:

- Contact you to discuss the incident that allegedly caused the injury or damage to the property

- Deal directly with the other party and/or attorney to handle the claim

Workers’ Compensation Claims

In the event an employee is injured on the job:

- Complete the Employer’s First Report of Injury or Disease form for all claims. Either use the “call in” reporting system or fax the original form to the insurance company.

- Forward a copy of the First Report to your broker in the event of a disabling injury or death claim. They should follow-up with the insurance company for their prompt handling of the claim.

- Contact the insurance company to question the status of a claim. If you experience delays or have questions, contact your broker for assistance.

After you report the claim to the insurance company, the claims adjuster will:

- Contact the injured employee to discuss the accident

- Request copies of bills and doctors’ reports for medical treatment administered

- Contact you, the employer, if there is any lost time from work as a result of the injury

Auto Insurance Claims

In the event of an automobile accident:

- Report the accident to the police.

- Obtain information about the other people involved in the accident such as:

- Names, addresses and phone numbers

- Insurance company

- Type of vehicle

- Auto and driver’s license numbers.

- Have your vehicle towed to the nearest repair shop if the vehicle is not drivable. Do not authorize repairs until the claims adjuster gives you the authority to do so.

- Call your insurance broker or carrier to report the accident.

In the event of a windshield, vandalism or theft loss:

- Report the vandalism loss or theft to the police.

- Call us to report a loss.

After the claim is reported to the insurance company, the claims adjuster will:

- Contact you to request details of the accident and repair estimates

- Arrange for an appraiser to inspect the damages of vehicles that are not drivable or extensively damaged

- Contact you for a settlement

- Deal directly with the others involved in the accident

You should not talk to others involved in the accident, but refer them to your claims adjuster.

-JK

Source: Zywave, Inc.

Small Business Insurance with The Hartford

Working as a broker, I work with a lot of different carriers on behalf of my clients to place their business insurance. One of the major carriers that I work with is The Hartford, an AM Best A (Excellent) XV ($2B or Greater Financial Size) rated carrier. The Hartford’s a great carrier to work with if you have a small business.

Interested in what they have to offer? Contact me anytime to discuss. Maybe we can find you something competitive backed by great coverage.

Here’s a new video featuring their focus on small businesses insurance.

-JK

Workplace Safety in the Restaurant

Last night I found the most horrifying commercial/ad ever on Youtube. It shows very graphically that Commercial Kitchens can be extremely dangerous places to work. It’s only an advertisement, but it’s a heavy message but I guess it served it’s purpose as it’s now scarred in my brain. See for yourself:

The pressure of service and working in a restaurant with dangerous equipment and products can have a serious impact on one’s livelihood. As a restaurant owner, it’s critical to maintain a safe workplace for your kitchen staff. Good communication between co-workers as well as understanding and following all workplace safety procedures are essential in preventing burn injuries in restaurants. To reduce your risk of suffering a scald burn injury or causing a co-worker to be burned, consider the following precautions:

- When you are manually transferring hot liquids, make sure the container is no more than half full, and use a lid or splash guard.

- When using a rolling cart to transfer hot liquids, check to be sure the container is secure on the cart so it will not tip or fall from sudden stops or jarring.

- Use extreme care when handling foods or liquids that have been microwaved, as they can reach temperatures greater than boiling without bubbling.

- Keep floors clear of liquids and debris. Slips, trips and falls are responsible for many restaurant scald burns, and often these injuries can result in more time lost at work than other scald injuries.

- When appropriate, use hot pads, pot-holders or proper gloves/mittens.

- Always wear protective shoes with slip-resistant soles – never open-toed shoes, sandals or boots.

- Follow all safety procedures when working with deep fryers.

*This information is for informational purposes only . It’s not intended as medical or legal advice

Source: Zywave, Inc.

-JK

15 Signs of Workers’ Compensation Insurance Fraud

Workers’ compensation fraud costs the insurance industry roughly $5 billion each year, according to estimates by the National Insurance Crime Bureau. And depending on whom you ask, fraud accounts for as much as 10% of the costs of all workers’ comp claims.

With the tougher economic times, particularly as lay-offs mount, we’ve definitely seen a trend in our agency of work-related injuries for a variety of manufactured reasons, such as for an injury that occurred on personal time.

Look for these tell-tale signs of potentially fraudulent claims. Usually one of these items alone is not enough to point to fraud, but if you have two or more of these signs, it could suggest a problem.

1. Late reporting. If you have an employee who suffers a legitimate on-the-job injury, they will generally report it right away. This may not always be indicative of a fraudulent claim, though, because sometimes the true effects of an injury may not be known until the following day.

2. The Monday morning claim. If the injury allegedly occurred on Friday, usually late in the day, but did not get reported until Monday, there is reason to suspect there might be a little more going on than meets the eye. The logic is that the employee likely suffered an injury over the weekend and does not want to pay for it themselves if they lack health coverage, or if they don’t want to foot the bill even for their health coverage deductible.

3. Lack of witnesses. Often your employees won’t be working in a solitary environment and there ought to be somebody on your staff who witnessed the accident. Still, not every claim has a witness and this should not be used solely to determine fraud.

4. Sketchy details or conflicting descriptions. Most claimants can recall the details of their injury. If the claimant seems to be fuzzy on the details and gives vague responses to questions, it could be a warning sign. Also, if the employee’s description of the accident conflicts with the medical history or First Report of Injury, there may be a problem. This could arise if, upon further investigation, the employee keeps changing the story and adding or removing pertinent information – a good reason to suspect it to be a fraudulent workers’ compensation claim.

5. Disgruntled employee. A disgruntled employee is more likely to place fraudulent claims than an employee with high job satisfaction.

6. Financial hardship at home. Workers’ compensation benefits are sometimes seen as a way out of a tight financial situation at home. Although temporary disability benefits are lower than normal working wages, the worker could use the time to “double dip,” that is, take on extra work when they are supposed to be at home recovering from the alleged injury.

7. Hard to reach. This ties in with number six. If this occurs every time the claimant is called, there is a possibility of fraud.

8. Misses medical appointments. If an employee is truly injured, they want to get better and will make sure to go to all medical appointments. Missing appointments is another reason to suspect fraud.

9. Employee is engaged in activities at home that are not consistent with the injury. If your employee reported a back injury and other employees find that he is playing softball on the weekends or renovating his yard, there is a good reason to suspect fraud.

10. Employment change. The employee reports the injury right before or after being laid off, near the end of a contract job or near the end of seasonal work.

11. Post-termination claims. If an employee files a claim after being laid off or fired, red flags should pop up.

12. Frequent moves and changes. The claimant has a history of frequently changing physicians, addresses and places of employment.

13. History of claims. If the claimant has filed suspicious or litigated claims in the past, they could be a person who feeds off the system.

14. Employee refuses treatment. There should be no reason that a legitimately injured worker refuses a diagnostic procedure to confirm the nature or extent of an injury.

15. Rigorous hobby. If the injured worker has a pastime that could cause an injury similar to the alleged work injury, the claim could warrant further investigation.

Remember, if you suspect fraud, you should talk to your broker or the insurance company claims representative to alert them. All insurance companies are required to have special investigations units that look into claims fraud. It benefits both you the employer and the insurer if the insurance company investigates and uncovers a fraudulent claim.

If the insurer suspects fraud, they can reject the claim and report their suspicions to the local district attorney’s office and the Department of Insurance.

Credit: Atlas General Insurance Services

About Me

I’m Jimmy Kinmartin, a California licensed Property & Casualty AND Accident & Health insurance agent/broker.

I grew up in Fullerton, CA and graduated from Servite High School in Anaheim. I have my Bachelors degree from Loyola Marymount University in Los Angeles. I currently live in Tustin, CA.

Please contact me if you need help with any of the following lines of insurance for your business:

-Cyber / Data Breach

-Commercial Property

-Commercial General Liability

-Products Liability

-Workers Compensation

-Commercial Auto

-Umbrella/Excess Liability

-Errors & Omissions/ Professional Liability

-Employment Practices Liability

-Directors & Officers

-Life & Disability Insurance